LIBOR is going away, but that’s sort of old news at this point. However, it has been received wisdom that only after the Bank of England stops imposing an obligation upon member banks to publish LIBOR quotes as at the beginning of 2021, would LIBOR go away and then we would need a replacement. That’s troubling, but of course most of us have plenty of other more immediate things to worry about between now and 2021. (NY Football Giant’s 2018 Season, impeachment, drone assassinations, hand size, etc.)

Here’s the deal. We’re not going to have all that time to get a LIBOR replacement right. It’s nightfall in our zombie movie and it’s always a bad sign when the mostly dead are shuffling about.

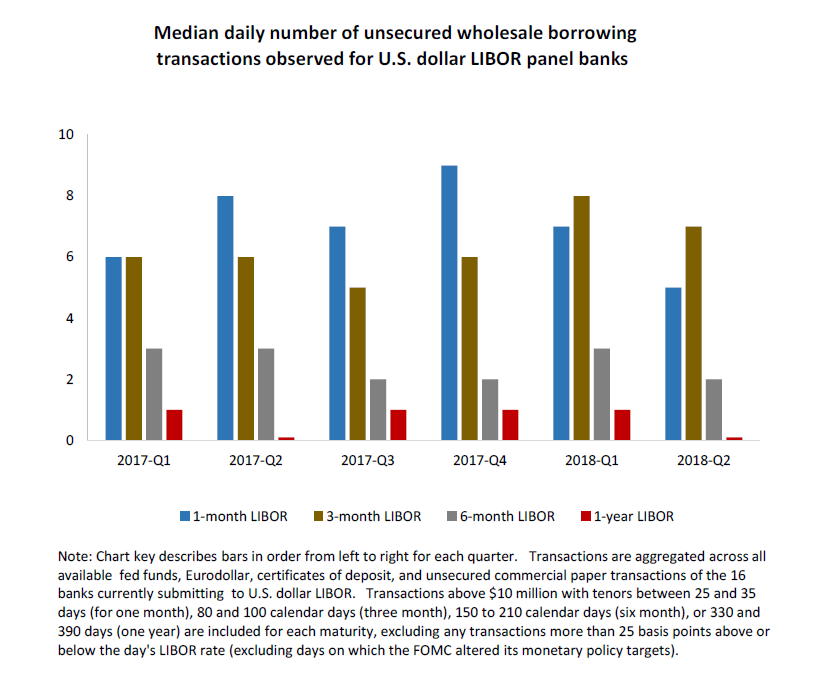

At the Alternate Reference Rate Committee (ARRC) Roundtable at the Federal Reserve Bank a couple of weeks ago, I, at least, was shocked to find out how breathtakingly thin the actual data behind LIBOR is day in and day out. Folks, it’s a $200 trillion market and the median daily number of actual borrowing transactions which are observable in the marketplace in Q2 2018 for 1-month LIBOR was five. Five, that’s not a typo. Five. Now, we’ve always known that LIBOR is a bit of a shell game where reporting banks generally report the interest rate that they would borrower at if they did borrow, but of course, they don’t. The LIBOR quotation process has always had a certain number of actually observed transactions floating like raisins in the rather odious blancmange of a made up data set, but only five actual quotations? We’re moving trillions of dollars of cash and synthetic product based on that little bit of real news?

{kind=link}

LIBOR has been in the news for quite a while, ever since we confronted the fact that it’s largely a fabulist invention. However, the focus has been on prosecuting traders who allegedly diddled the process (Diddling data fields which, in the first instance are entirely made up, is sort of an interesting thought exercise, don’t you think? Can you fake, fake news?) Maybe justice must be served, but in the great scheme of things that was a distraction. If we end up with a sloppy end of LIBOR without a transition to a new reference rate, it will be bad. This is not Y2K.

We have a process underway designed to replace LIBOR. It’s deliberative and it’s gradualist and it’s linear. At the ARRC roundtable, Fed officials even bragged that we’re about six months ahead of the schedule they set in their Paced Transition Plan, but remember that Plan contemplates the presumed successor to LIBOR will only be available on January 1, 2021. Taking just in time inventory just a bit too far if you ask me. This effort will be frustrated by a disorderly early collapse of LIBOR. We need to take that risk seriously.

I’ve been saying in this commentary for some time that I thought a significant risk here was that LIBOR would go away before 2021 because it’s simply not a reliable measurement of any reality. Now, that we have been forced to confront the fact, it should be almost intolerable to continue to rely upon this reference rate. How do we justify waiting for 2021?

Andrew Bailey, the head of the UK Financial Conduct Authority (FCA) that is responsible for overseeing LIBOR, said in July that the FCA could declare LIBOR nonrepresentative if it thought LIBOR was no longer a reliable basis to benchmark trillions of dollars of transactions. No longer reliable? Was it really ever? If the FCA declares LIBOR nonrepresentative then, under the EU Benchmark Regulation, supervised firms in the European Union, including financial institutions, exchanges, trading facilities and clearing houses, would only be able to use LIBOR for legacy contracts and not new business. The Federal Reserve Vice Chairman for Supervision Randal Quarles in his prepared remarks at the ARRC meeting directed markets to take note. Read the tea leaves folks: LIBOR is not making it to 2021. And the only thing worse than a disorderly handoff from LIBOR to SOFR on a date certain is to have LIBOR and SOFR both published and used in tandem for a considerable period of time. Can you imagine the dissidence in the borrower and counterparty community when efforts are made to switch to SOFR under these circumstances? Winners and losers will abound. Call the trial lawyers!

This all is very troubling because notwithstanding all of the committees, task groups, study groups and industry forums that have been organized to think about LIBOR, there’s very much more sound and fury than light right now. We’re still fixing to address the problem with the sort of desultory absence of urgency long associated with southern climes. A good process is fine when the risks are at a certain remove, but we no longer have that luxury. The silver is all lined up neatly in the silver chest and all the chairs are put away, but we’re still on the Titanic.

We need an executable plan for LIBOR replacement now. We need a plan that could be implemented as early as next year. We’re not going to get any smarter. It’s time to stop studying and start doing. We need to make decisions.

While there may be other runners still in the game, the Secured Overnight Financing Rate or SOFR, a rate derived from overnight repos of treasuries seems the consensus choice as the basis for the new reference rate. In some quarters, alternatives are still being considered. This should stop. SOFR is already trading in a semi-robust way and producing real pricing from real trades. Shocking! We’ll actually price financial assets off real trades. Let’s embrace SOFR and move on.

We’ve had some very productive conversations about how SOFR, an overnight, largely riskless rate, can be utilized to determine term rates and how to address a riskless rate as a reference rate. Industry groups have come up with a pretty good answer. We will use a hierarchy of SOFR derived rates based on what’s available at that time. If we have published term SOFR, fine. We’ll use that (maybe we will have a term SOFR sometime in early 2020…maybe). If we don’t have term SOFR, then we’ll use interpolated term SOFR. This could be derived from a futures product that exists now and is likely to grow more robust over the next few years. If neither of those exist, we use spot quotes or average spot quotes. Not perfect but it’s an answer.

There is lots of palaver on what triggers the swap out of SOFR for LIBOR. There are two important questions here. The first is when and the second is who says. On the first, there are institutions saying we need to phase SOFR in over a considerable period of time but others say we need a hard date or a date certain. I don’t know the right answer here, but we need to get that nailed down. None of these options are perfect, but it’s likely that all can be made to work.

Who drops the flag and commences the race to transition? Will it be the Treasury? Do we switch when the prudential regulators tell the banking community that it’s no longer prudent to price assets off LIBOR? Maybe we should take our lead from the GSE’s. Can we have industry groups get together and decide when to do it? I don’t know the answer, but again – all will work. No choice is perfect but we need to decide and decide now.

We’ve had lots of conversations about how to spread adjust SOFR to reflect something that looks like current LIBOR. Remember LIBOR is a rate that has economic risk baked into it. SOFR does not. How do we adjust one to look like the other? This is an important question for the legacy book, which no matter how many folks try to dismiss it as a real problem, remains a very real problem, and will continue to grow as a problem until the new rate is fully implemented. Pick something and stick with it.

Finally, we are talking about the fact that our Zombie LIBOR may get even more zombie-like before we’re done. A zombie of a zombie, if you will. As mentioned above, it may be that LIBOR remains viable for legacy deals through 2021 while SOFR is used for new deals. All of which may be happening against a backdrop of various regulators essentially continuing LIBOR, a no longer reliable reference rate. One shudders to think of the chaos when borrowers are confronted with their lenders purporting to change the interest rates on their loans by using SOFR when something called LIBOR is still being published and used. Wash, dry, fold and repeat! Call the trial lawyers!

We also need to talk about operational difficulties. In my securitization world, no one has adjusted the data collection or data transmission medium to account for a new index rate, a new spread and a new interest rate. No one is really certain who will make the decision in securitization. No one has really comprehensively reviewed their book to see what their existing alternate rate language is, let alone begin to install uniform industry-wide alternate rate language.

Progress has been made, but we’re nowhere near ready. Look, unless we’ve decided to have the government somehow legally mandate a switch out of one rate into another, which seems both inadvisable and frankly, impossible, the decisions to change the reference rate are going to be deal by deal, instrument by instrument, participant by participant. At best, that screams chaos. However, if large segments of the market could move quickly and decisively to embrace a general consensus around the half dozen critical questions discussed above, some of that might be avoided.

Did you happen to see the FT’s article from Sunday, August 5th entitled “Banker warns of Herculean task to escape Libor’s tentacles” by Joe Rennison and Robin Wigglesworth? This article highlighted the problem that as our committees and study groups, bureaucrats and Wall Street types have been beavering away at the LIBOR problem, an awful lot of folks in the financial marketplace writ large have not yet noticed that LIBOR is going away. Are all mortgage bankers, borrowers, service providers, the folks at our 7,000 sub-regional banks paying any attention? Right now, recognition of the problem and the thinking about the fix seems to be largely confined to a small coterie of money center banks, major investors and Wall Street players. That won’t work. Even if we declare victory and agree on a new reference rate, agree on when the reference rate should be swapped in, agree on how to calculate that rate, agree on who tells us when the transfer will occur, it will be chaos unless the vast majority of participants in the financial marketplace are really tuned into the change and ready to move. If we had two plus years to educate about the orderly transition to SOFR that might not be a terrible thing here in the dog days of summer 2018, but if I’m right and LIBOR is going away sooner, this lack of understanding across the marketplace about when LIBOR falls will greatly exacerbate the problem.

All that is a heavy lift and while, if we had two and a half years more to get this right then we probably would. But now, I don’t think that’s true. My guess is that someone is going to announce the emperor’s got no clothes and LIBOR is an inappropriate reference rate for market transactions sooner than that, and in that case those chomping zombies will be among us with a vengeance.

What’s to be done? Accelerate the process of getting to a solution. Eliminate self-congratulations for a good inclusive process, start to scramble for a solution and educate the markets. If we don’t have a pretty good handle on a solution by the end of 2018, shame on us.